Trump seeks 43% cut to HUD in 2026 budget plan

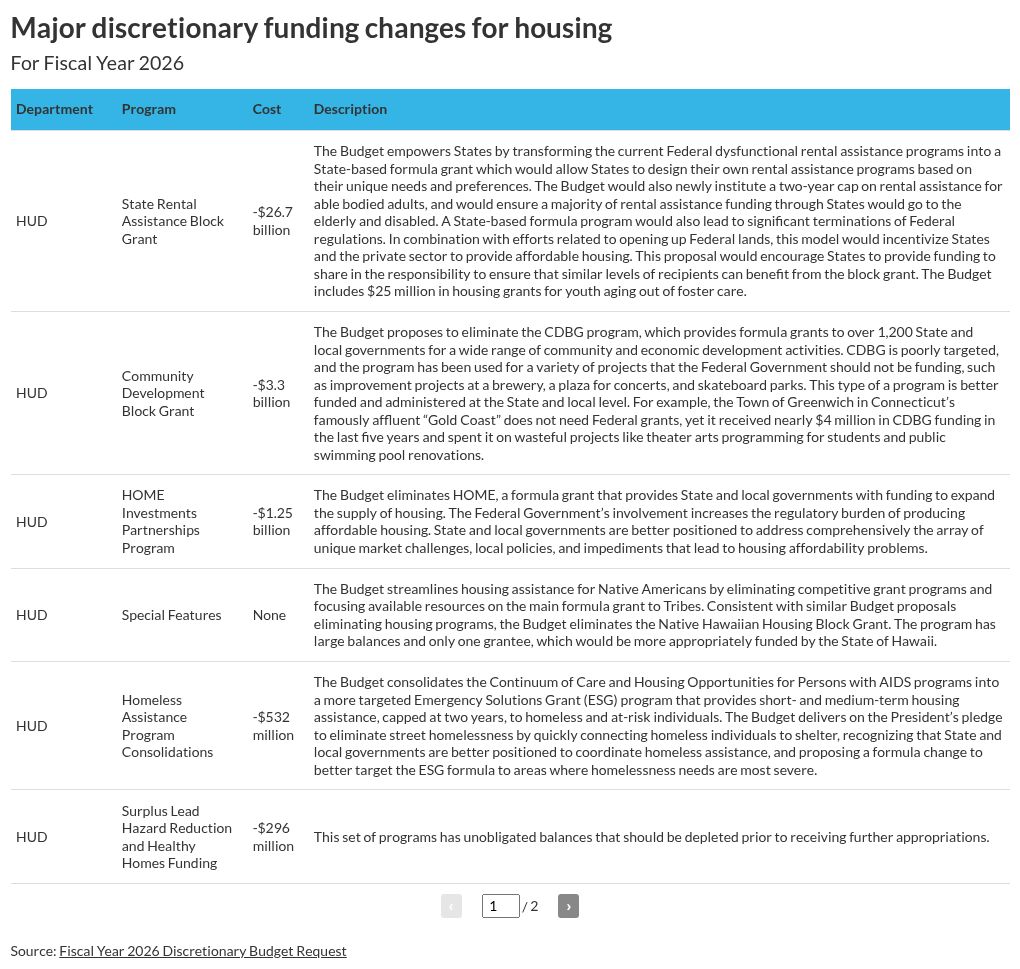

unitedbrokersinc_m7cmpd2025-05-02T21:22:29+00:00The Trump administration wants to cut the Department of Housing and Urban Development's budget by 43.6%, a reduction that would require eliminating some programs. The recommendations for discretionary funding for fiscal year 2026 released Friday propose slashing HUD's budget from $77 billion in FY25, to $43.5 billion in FY26. The potential $33.6 billion reduction is part of a push to pass responsibility to state and local governments, and to eliminate spending that's "contrary to the needs of working Americans," wrote Russell Vought, director of the Office of Management and Budget and current acting director of the Consumer Financial Protection Bureau.HUD Secretary Scott Turner in a statement Friday afternoon said the recommended budget cuts will thoughtfully consolidate and streamline existing programs. "Importantly, it furthers our mission-minded approach at HUD of taking inventory of our programs and processes to address the size and scope of the federal government, which has become too bloated and bureaucratic to efficiently function," he said. The budget suggestions follow moves by President Trump's cost-cutting task force to eliminate over 100 vendor contracts at HUD for a stated savings of at least $130 million. The department has repeatedly touted $260 million in savings and the recovery of $1.9 billion in "misplaced" funds, which have since been revealed to be master subservicing line items. HUD in a separate statement Friday touted its work with the Department of Government Efficiency to cut fraud, waste and abuse. That acknowledgement came in response to an inquiry regarding a Wired report alleging that a college student was using artificial intelligence to propose rewrites of HUD regulations. A spokesperson said HUD doesn't comment on individual personnel. See the full list proposed housing changes in the table at the end of this story.Proposed changes at HUDThe largest cut suggested in the Trump budget proposal is a $26.7 billion reduction to HUD's "State Rental Assistance Block Grant," which provides funding for rental assistance, public housing, elderly and disability housing. The proposed budget would use a state-based formula grant in lieu of a "dysfunctional" federal system. The budget would also place a new 2-year cap on rental assistance for able-bodied adults. HUD is also looking to eliminate its $3.3 billion Community Development Block Grant, suggesting funds have been poorly targeted. The budget cites improper funding for improvement projects for a brewery, a concert plaza and skatepark. The government is also proposing to eliminate the HOME Investment Partnerships Program, another formula grant to fund the expansion of housing supply. Other nine-figure cuts include slashes to Native American Programs and a cost-cutting consolidation of Homeless Assistance Programs. A $100 million Pathways to Removing Obstacles program is on the chopping block for advancing "'equity' under the guise of an affordable housing development program."HUD emphasized that it is maintaining support for its Fair Housing Assistance Program, which funds state and local agencies responsible for processing 80% of the nation's fair housing complaints. At the onset of the Trump administration, HUD's fair housing enforcement operations were reportedly considered for layoffs. CDFI Fund changesThe Trump administration is also calling for changes to the Community Development Financial Institutions Fund, a collection of federally mandated programs that aid underserved borrowers. The budget calls for a $100 million increase for a new Rural Financial Award Program, which would require 60% of CDFI Fund loans and investment to go to rural areas. At the same time, the Trump administration calls for a $291 million reduction to CDFI Fund discretionary awards, citing past awards' focus on racial equity and climate resiliency. "The CDFI industry has matured beyond the need for "seed" money and should at this point be financially self-sustaining," the budget said.