Two and Roundpoint eye opportunities for diversification

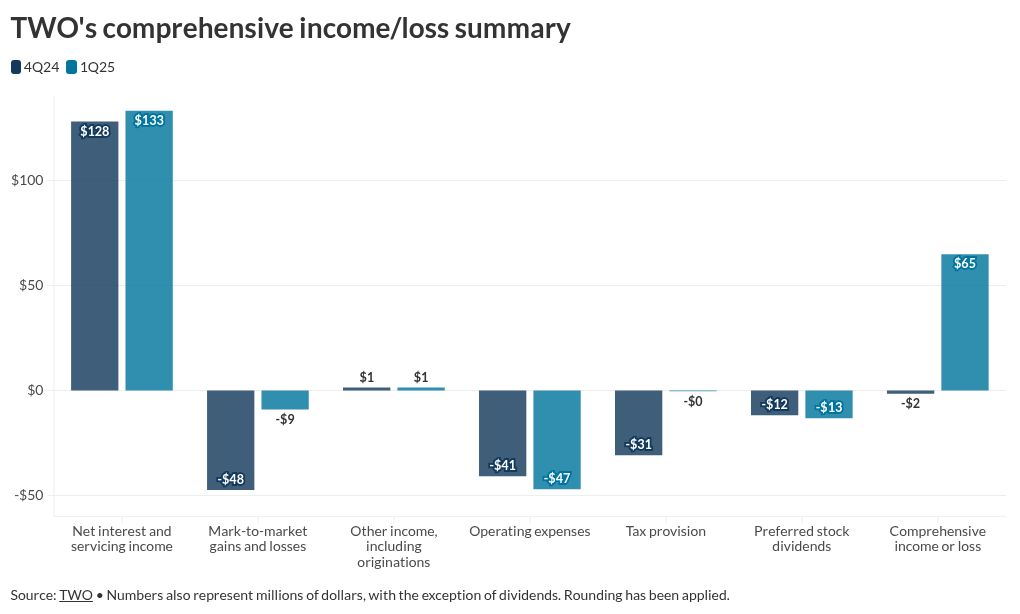

unitedbrokersinc_m7cmpd2025-04-29T15:22:38+00:00Two, the real-estate investment trust that owns Roundpoint Servicing, is considering more expansive moves for its mortgage business lines as persistent volatility in the capital markets presents a mix of challenges and opportunities for its investments.The company formerly known as Two Harbors Investment Corp. recorded a first quarter loss of $92.24 million under standard accounting principles, compared with net income of $264.95 million the previous quarter. However, Two's comprehensive income was a positive $64.93 million compared to a loss of $1.62 million the previous quarter. The company reported $25.09 million in earnings available for distribution for the latest period, compared to $21.18 million in EAD the previous quarter."While overall spreads have widened in the second quarter, they have been variable day-to-day, and we have actively managed the portfolio and our risk to take advantage of any market dislocations," President and CEO Bill Greenberg said during the company's earnings call.Two's diversification strategyGreenberg said the company's goals for 2025 center on activities that diversify beyond its investments in agency securitizations and mortgage servicing rights.These include "fully scaling" its direct-to-consumer origination platform, an expanded presence in the subservicing market, and product set expansion in second lien, Ginnie Mae and non-agency markets."We view the Roundpoint platform as an expansion of our opportunity set, providing additional benefits for our shareholders," Greenberg said.When asked about the impact of the planned combination of industry giants Rocket Mortgage and Mr. Cooper, Greenberg said he viewed it as most likely to make the bid for MSRs "a bit more competitive that it was at the margins."Greenberg confirmed during the call that William Dellal has been promoted to permanent chief financial officer from acting CFO. Dellal previously had planned to resign but the company announced a change of plans earlier this month.Chief Investment Officer Nick Letica said in a press release there have been upsides for Two as the market's volatility has widened spreads on agency mortgage-backed securities that the REIT invests in and boosted levered returns on the bonds.Outlook on mortgage servicingHe added that the company's investment in mortgage servicing rights should remain stable because its portfolio has lower coupons, protecting it from the risk borrowers will refinance into lower interest rates and cause runoff.Net interest and servicing income improved on a consecutive-quarter basis, rising to a rounded $133 million from $128 million. The mark-to-market loss for the period fell to $9 million from $48 million. Other income, a category that includes earnings from originations, was stable at $1.4 million for both quarters. Operating expenses increased to $47 million from $41 million.The REIT settled flow-sale acquisitions of mortgage servicing rights with an unpaid principal balance of nearly $175 million during the quarter. The REIT reported that after the fiscal period ended, it committed to buy two bulk packages of MSRs with a UPB of $1.7 billion.Analyst consensus was generally that Two's bottom line was weaker than anticipated, but its revenue outperformed expectations and its stock price was wavering but generally trending upward immediately after its earnings call on Tuesday morning.Its shares had opened at $12.30, dropped to $11.70 then rebounded to $12.43 at deadline.